Blue Sky Institute

Preamble

In order to do their part in advancing the welfare of all life, the founders of the Blue Sky Institute (BSI) originated and have expanded its programs over a period of time that has spanned from early in January of 2000 to the present. Since then BSI has increased its Board of Trustees and volunteers in its various projects and initiatives. It is the intent that the BSI will indefinitely exist to further it’s mission to Advancement of the Welfare of all life thru continuing to design, develop and implement BSI’s Educational Programs and Projects.

The Founding of an Educational Organization to allow the most effective achievement of the objective of promoting such “advancement” involves several justifications and also many legal complexities. The justifications for helping create an Educational Organization structure are simply put, to have the deserved tax exemption status that such a structure can allow, for the collection and utilization of resources to allow for the implementation of Projects and Programs of an Educational nature. The other major justification for Blue Sky Institutes formation is to create an Enduring tool to allow people to help other people to live better lives thru Education.

Incorporating with the State and Other Legal Matters

INCORPORATING

The process of “Incorporating” is essential in this society in order to obtain “Recognition of Exempt Status under 501(c)(3) of the Internal Revenue Code” which is essential for obtaining grants and other contributions from various sources that can be utilized for furtherance of Education.

The Articles of Incorporation were created by the founders, who volunteered their time and other resources such as office supplies to the project of Incorporating thereby eliminating need to pay any fees other than those required by law to achieve the objective of Incorporation.

On the Thirteenth of December 2000 the Articles of Incorporation of Blue Sky Institute were submitted for registration with the Utah State Department of Commerce, Division of Corporations & Commercial Code.

On the Sixteenth of January 2001, the above named Division sent a notice of Incomplete Registration to our office. This notice was received at Blue Sky Institute on the 20th of January 2001. The notice stated in a bold face all caps format the following “YOU MAY NOT USE THE WORD INSTITUTE IN THE CORPORATE NAME” and very little else was written into the “Incomplete Registration” form. Since the founders did not understand the ‘why’ of it, they looked into the “Utah Code” and found out that they were able to use the word “Institute” as part of the corporate name if the “written consent from the Utah State Board of Regents”. was obtained. The “consent” was obtained and the founders were informed that the “Certificate of Registration” had been printed, and Blue Sky Institute has been registered in good standing as a Utah Non-Profit Corporation since.

TAX EXEMPTION

In order to obtain funding for: the purchase of Educational Materials, paying of Educator Compensation, and providing proper facilities for Educational Projects and Programs; contributions and gifts will be accepted by BSI. As with other organizations that provide beneficent services and goods for “Charitable Purposes” (defined as many different types of services including Education), BSI qualifies for Exemption from Income Taxation as well as exemption from some certain other Taxes. Please refer to the page describing our Policy regarding the Ethical Utilization and Disbursement of Resources obtained thru contributions and Grants which is a formalization of our intent to have all contributions be used for the purpose of Education.

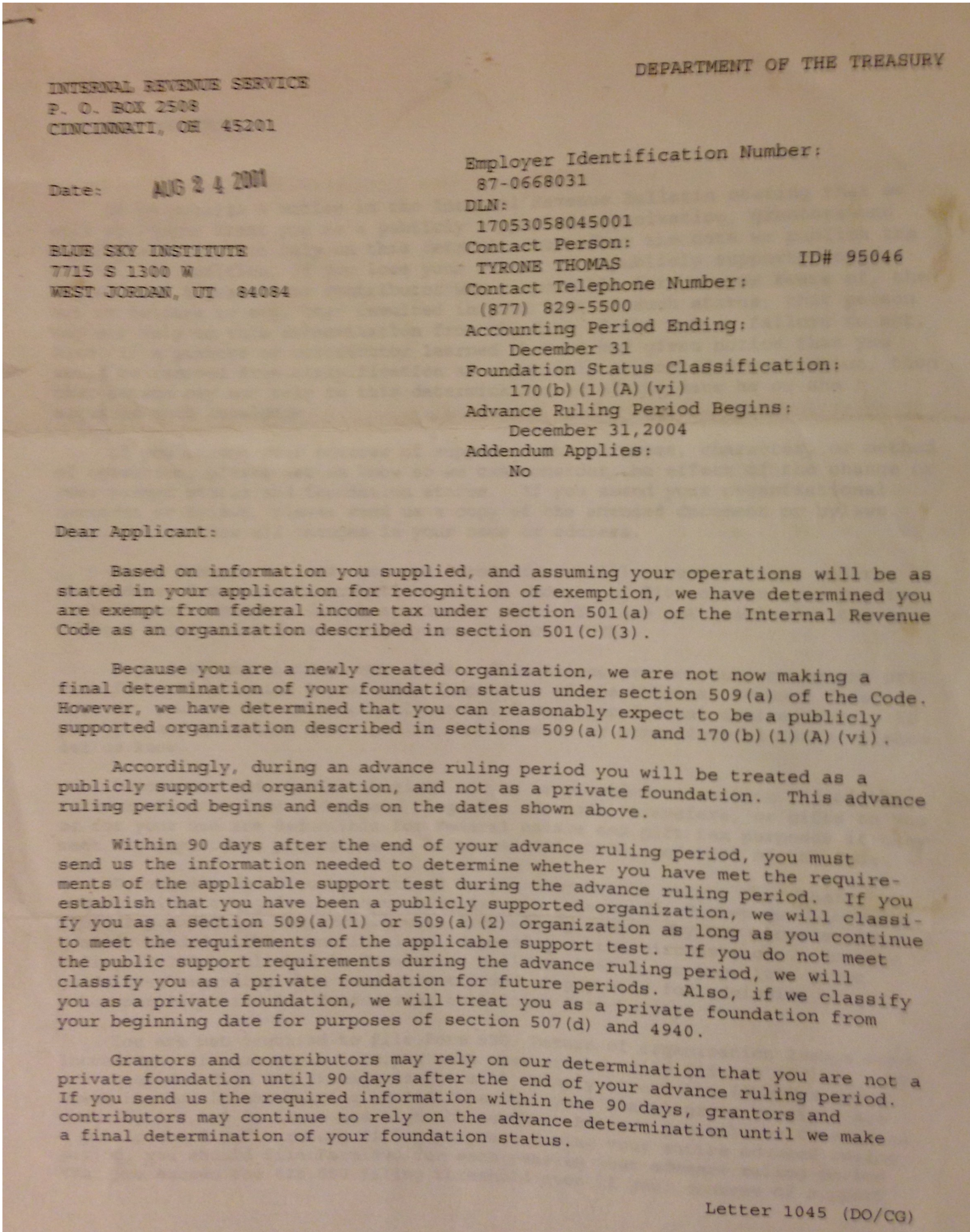

Letter of Determination

The Letter of Determination from the IRS was received in August of 2001.